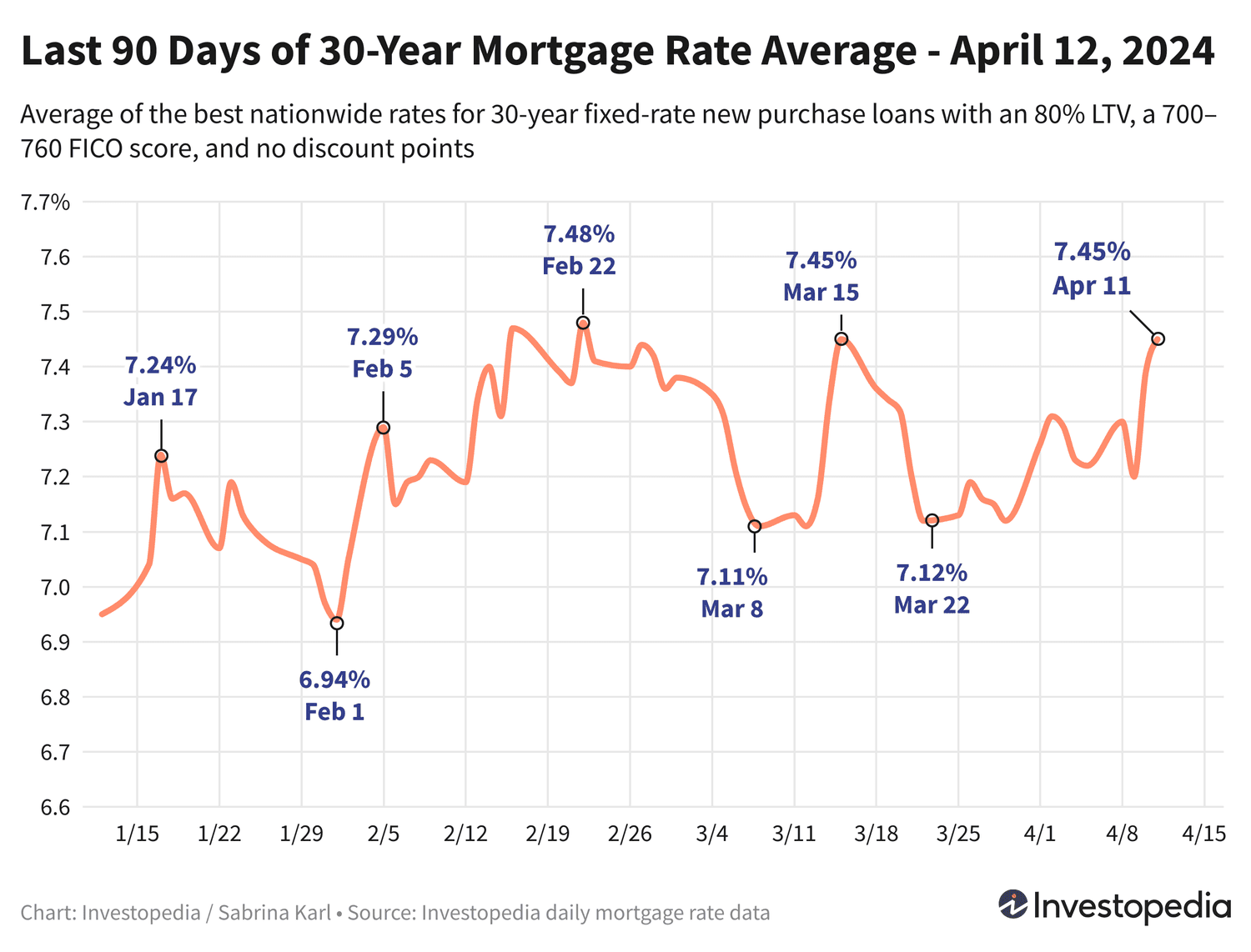

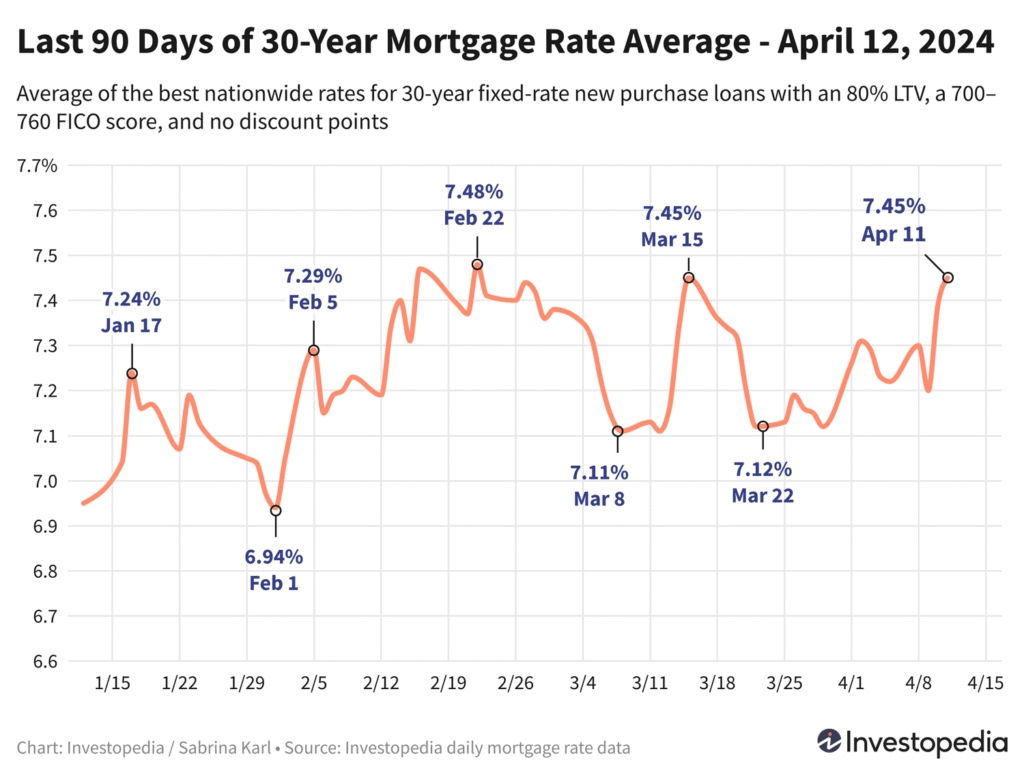

When most UK homebuyers check mortgage rates, they assume the numbers move in a simple, predictable way—usually tied directly to the Bank of England’s base rate. But that assumption misses a deeper and more important truth: mortgage rates are influenced by a web of financial forces that go far beyond central bank decisions.

Understanding these hidden drivers can give buyers and remortgagers a real edge—especially in volatile markets like the one we’ve seen in recent years.

The Bank Rate Is Just the Starting Point

Yes, the Bank of England base rate matters. It directly affects tracker mortgages and influences lender pricing. But fixed-rate mortgages—the most popular option in the UK—aren’t based on today’s base rate alone.

Instead, lenders price fixed deals based on expectations of future interest rates. This means mortgage rates can rise even when the base rate hasn’t changed—or fall before any official cut happens.

Swap Rates: The Real Engine Behind Fixed Mortgages

If you want to understand UK mortgage pricing, you need to look at swap rates.

Swap rates are essentially the interest rates that banks pay to borrow money over a fixed period (like 2, 5, or 10 years). These rates are driven by market expectations—especially inflation and economic growth.

When swap rates rise, mortgage lenders’ costs increase. That cost gets passed on to borrowers through higher fixed-rate deals.

This is why, during periods of economic uncertainty, mortgage rates can jump quickly—even without a base rate change.

Inflation Expectations Matter More Than Inflation Itself

A common mistake is focusing only on current inflation figures. In reality, lenders care more about where inflation is going.

If markets believe inflation will stay high, lenders will price mortgages higher to protect themselves. Conversely, if inflation is expected to fall, mortgage rates may drop in advance.

This explains why mortgage rates sometimes decline even when inflation is still above target—the market is forward-looking.

Global Influences on UK Mortgage Rates

Mortgage rates in the UK aren’t purely domestic. Global financial markets play a major role.

For example:

- US interest rate policy often impacts global bond markets

- Geopolitical instability can drive investors toward safer assets like government bonds

- Currency fluctuations affect investor confidence in UK markets

All of these factors influence swap rates—and therefore mortgage pricing.

Lender Competition: The Underrated Factor

Even when funding costs rise, lenders don’t always pass everything on to borrowers.

Why? Competition.

In a crowded mortgage market, lenders often cut margins to attract business. This is why you’ll sometimes see “rate wars,” where major banks and building societies undercut each other.

For borrowers, this means timing matters. A slight shift in competition can create short windows where deals are unusually attractive.

Why Mortgage Rates Move Faster Than You Expect

One of the biggest frustrations for buyers is how quickly mortgage rates can change.

This happens because lenders adjust rates based on market movements, not just official announcements. If swap rates spike in the morning, lenders may pull deals by the afternoon.

In fast-moving markets, delays—even of a few days—can cost borrowers significantly.

The Impact of Government Policy

Government decisions—especially around housing—can indirectly affect mortgage rates.

Policies such as:

- Stamp duty changes

- First-time buyer schemes

- Housing supply initiatives

These don’t directly change rates, but they influence demand. Higher demand can push lenders to adjust pricing strategies.

Fixed vs Tracker: Choosing in Uncertain Times

Understanding rate drivers can help borrowers choose between fixed and tracker mortgages.

Fixed rates offer certainty, which is valuable when rates are expected to rise or remain volatile.

Tracker mortgages, on the other hand, can be cheaper initially—but expose borrowers to future increases.

The right choice depends on your risk tolerance and your view of where rates are heading.

What UK Borrowers Should Do Right Now

Instead of trying to perfectly “time the market,” borrowers should focus on preparation:

- Get a mortgage agreement in principle early

- Monitor swap rate trends (not just headlines)

- Be ready to act quickly when good deals appear

Speed and awareness are more valuable than prediction.

Final Thoughts

Mortgage rates in the UK are shaped by a complex mix of expectations, global markets, and competition—not just the Bank of England.

Buyers who understand these forces are better positioned to secure strong deals and avoid costly delays.

In a market where rates can change overnight, knowledge isn’t just power—it’s savings