Choosing between a fixed-rate and variable mortgage is one of the most important financial decisions UK borrowers face. Yet most advice simplifies the choice into a basic question: “Do you want certainty or flexibility?”

That framing is incomplete.

In reality, the decision should be based on a structured evaluation of economic conditions, personal risk tolerance, and financial positioning. This article breaks down a more strategic way to approach the choice in 2026.

Why This Decision Matters More Now

In stable markets, the difference between fixed and variable mortgages can be marginal. But in volatile environments—like the current UK landscape—the gap can be significant.

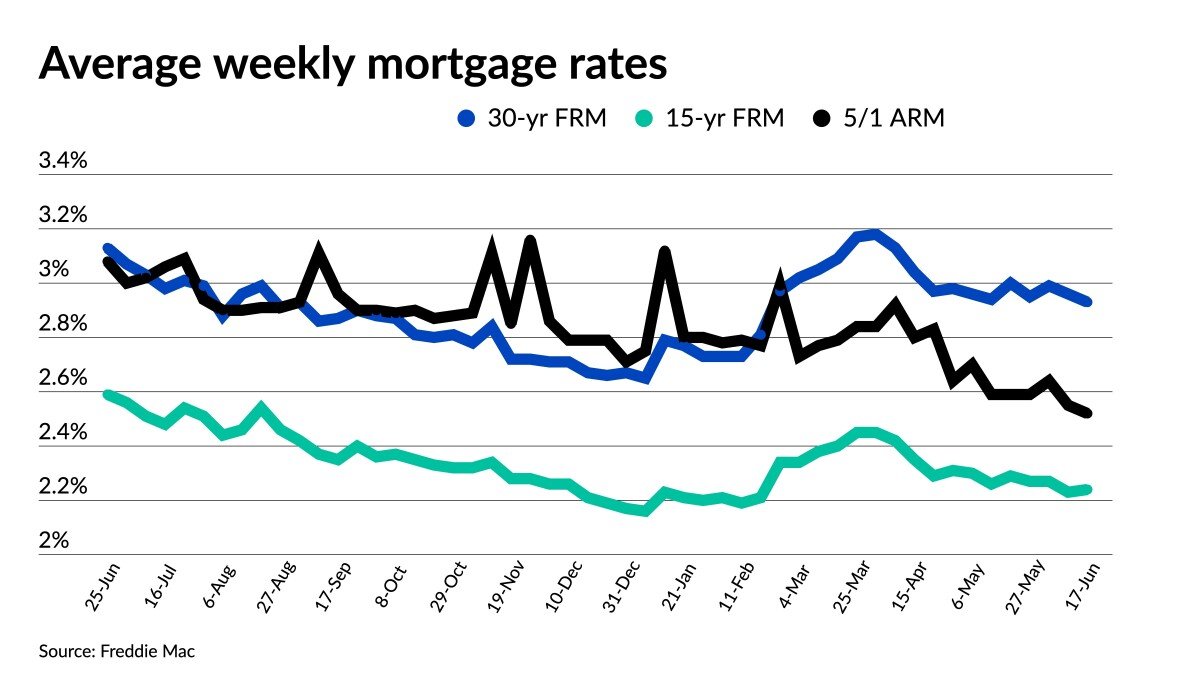

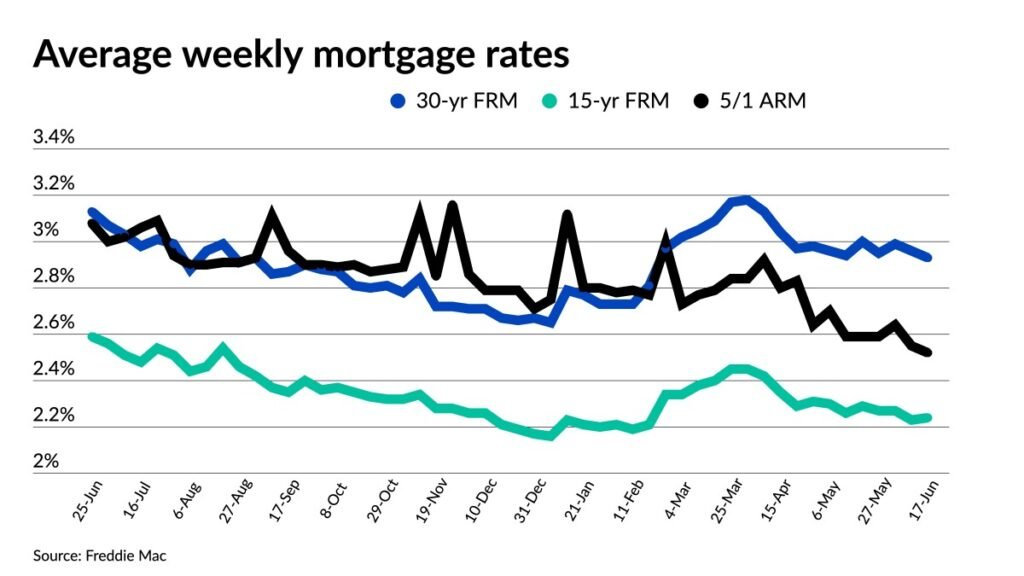

Interest rates have fluctuated sharply in recent years, and future movements remain uncertain. That uncertainty makes choosing the right mortgage structure more critical than ever.

Understanding Fixed-Rate Mortgages

A fixed-rate mortgage locks your interest rate for a set period—commonly 2, 3, 5, or 10 years.

Advantages:

- Predictable monthly payments

- Protection against rising interest rates

- Easier budgeting

Disadvantages:

- Higher initial rates compared to some variable deals

- Early repayment charges (ERCs) if you exit early

- Limited flexibility

Fixed rates are essentially a form of insurance—you’re paying for stability.

Understanding Variable Mortgages

Variable mortgages include tracker mortgages and standard variable rates (SVRs).

Trackers follow the Bank of England base rate, usually with a set margin (e.g., base rate + 1%).

Advantages:

- Often lower initial rates

- Potential to benefit from falling interest rates

- More flexibility in some cases

Disadvantages:

- Payments can increase unpredictably

- Exposure to interest rate volatility

- Budgeting becomes harder

Variable mortgages are a bet on future rate movements.

A Strategic Framework for Choosing

Instead of asking “fixed or variable,” consider these four factors:

1. Rate Direction Expectations

If you believe rates will rise or remain high, fixing can protect you.

If you expect rates to fall significantly, a variable mortgage could save money.

But be cautious—markets often price in expectations ahead of time.

2. Financial Resilience

Can you afford higher payments if rates increase?

If your budget is tight, a fixed rate provides security. If you have surplus income, you may be able to absorb fluctuations.

3. Time Horizon

How long do you plan to stay in the property?

Short-term owners may prefer flexibility, while long-term homeowners often benefit from locking in certainty.

4. Risk Tolerance

This is often overlooked.

Some borrowers are comfortable with uncertainty. Others value peace of mind above all else.

There’s no “correct” answer—only what fits your financial psychology.

Hybrid Strategies: The Overlooked Option

Many UK borrowers assume they must choose one approach. In reality, hybrid strategies can offer a balance.

Examples include:

- Fixing for a shorter term (e.g., 2 years) to retain flexibility

- Overpaying on a variable mortgage to reduce risk

- Splitting borrowing across different products (where available)

These approaches can reduce exposure while keeping options open.

Timing the Market: A Risky Game

Trying to perfectly time mortgage decisions is extremely difficult.

Even professionals struggle to predict interest rate movements consistently. Instead of chasing the “perfect” moment, focus on securing a deal that works under multiple scenarios.

The Role of Remortgaging

Remember: your choice isn’t permanent.

Most borrowers remortgage every few years. This means your current decision should be viewed as part of a longer-term strategy, not a one-off gamble.

Flexibility today can position you better for future opportunities.

Common Mistakes UK Borrowers Make

- Fixing purely out of fear without considering long-term costs

- Choosing variable rates without a buffer for payment increases

- Ignoring fees and focusing only on headline rates

- Delaying decisions and missing favourable deals

Avoiding these mistakes can save thousands over the life of a mortgage.

What’s Different in 2026

The current environment is shaped by:

- Persistent inflation concerns

- Uncertain economic growth

- Global financial instability

This makes flexibility and awareness more valuable than ever.

Final Thoughts

The fixed vs variable decision isn’t about right or wrong—it’s about alignment.

Align your mortgage with your financial situation, your outlook, and your tolerance for risk.

In a market defined by uncertainty, the best choice is the one you can comfortably live with—regardless of what happens next.